Healthcare’s Shifting Sands: Tech Investment Surges Past $110 Billion

Table of Contents

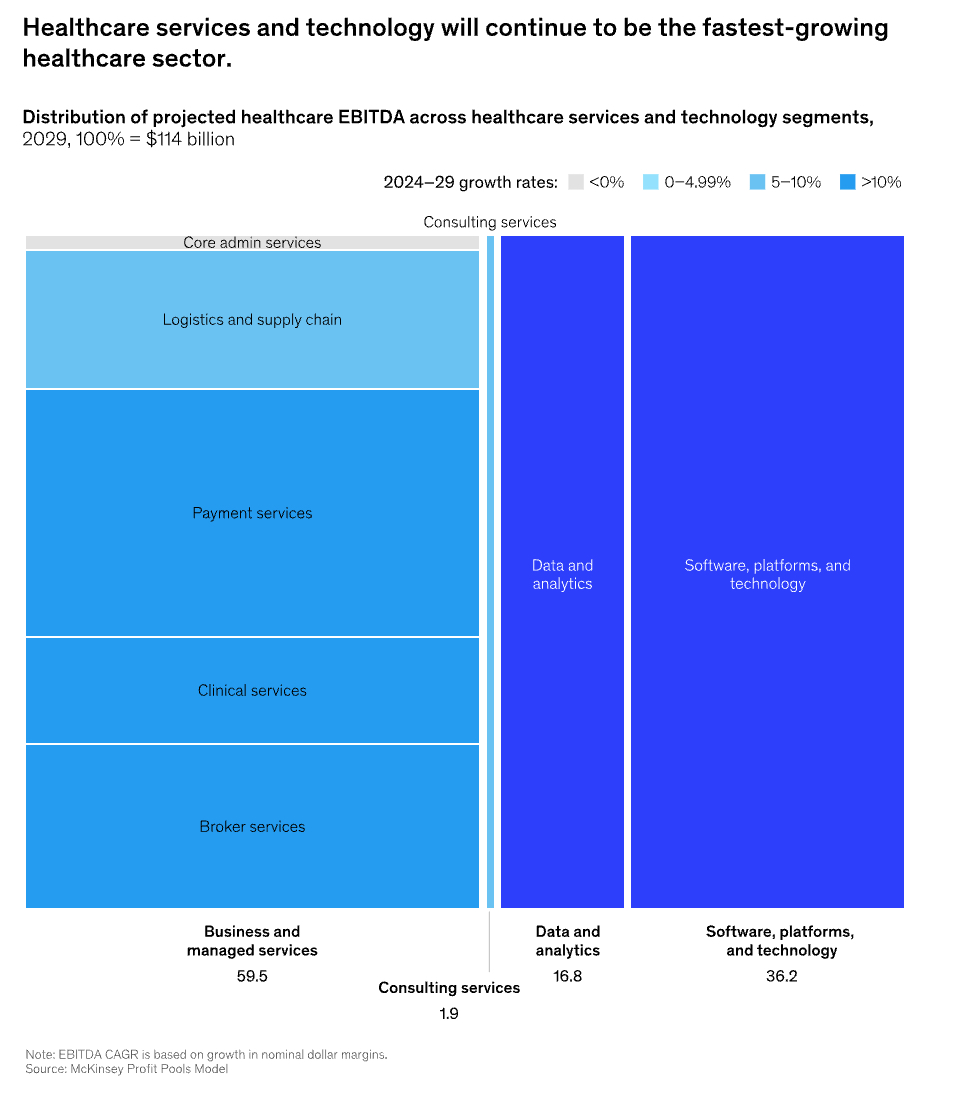

A new report reveals Health Services Technology is now the fastest-growing segment in U.S. healthcare.

- Health Services Technology (HST) is projected to exceed $110 billion in EBITDA by 2029.

- Customary healthcare providers and insurers are increasingly investing in AI and outsourcing.

- Generative AI adoption is accelerating, with 85% of healthcare organizations currently implementing solutions.

The U.S. healthcare landscape is undergoing a dramatic change, with investment in Health Services Technology (HST) poised to eclipse $110 billion by 2029. This isn’t just incremental change; it’s a essential shift in where the money flows within the industry.

An Uneven Recovery

The U.S. healthcare industry is navigating an “uneven recovery,” where hospitals and insurers are seeing their share of profits diminish as technology companies gain ground. A recent report indicated that industry EBITDA as a share of National Health Expenditure decreased from 11.2% in 2019 to 8.9% in 2024. Despite this overall downturn, HST stands out, poised for an impressive 9% annual growth through 2029. This represents a structural move of value from labor-intensive services to software and data analytics.

The Rise of Generative AI

The hype around Generative AI has given way to tangible results.The data demonstrates a notable acceleration in adoption rates: a striking 85% of healthcare organizations are currently implementing Gen AI solutions. Furthermore, over 10% of U.S. physicians are already leveraging AI-powered ambient documentation tools, like medical scribing, to streamline their workflows. This shift is particularly noticeable in areas with high administrative burdens, such as automated claims management and real-time data connectivity, where the return on investment is readily apparent.

Winners and Losers Through 2029

The report paints a clear picture of where financial gains will be concentrated in the coming years.

- providers: Facing a “fragile recovery” through 2027, hospitals are grappling with increasing uncompensated care risks due to ongoing Medicaid disenrollment. Though, non-acute care settings-including Ambulatory Surgery Centers, Home Health, and Hospice-continue to demonstrate strong performance.

- Payers: Group commercial insurance is becoming a “critical stabilizer,” expected to represent 36% of total payer profits by 2029 as individuals leaving Medicaid transition to employer-sponsored plans.

- Pharmacy: The market is being reshaped by the impact of GLP-1 drugs. These medications accounted for half of the 11% increase in drug spending in 2024, and total drug expenditure is projected to reach $1 trillion by 2029.

The Efficiency Trap

For years, the promise of technology reducing healthcare costs has remained largely unfulfilled. however, the data suggests that the current economic pressures, combined with the maturity of AI technology, are finally creating the conditions for meaningful change. But a word of caution: the real competitive advantage won’t come from simply owning AI, but from seamlessly integrating it. Vendors capable of connecting fragmented data silos will thrive, while those offering isolated “point solutions” are likely to be absorbed into larger platforms.

Key Takeaways for Healthcare Leaders

for healthcare ceos and CFOs, this report underscores that HST is no longer a secondary expense; it’s a core driver of growth.

1. Prioritize Outsourcing: Achieving scale efficiencies is increasingly difficult for mid-sized organizations to accomplish internally.

2. Double Down on ASCs and Home health: The shift towards alternative care settings is permanent and accelerating.

3. Audit your AI Roadmap: if your organization isn’t among the 85% implementing Gen AI, you risk falling behind the competition.