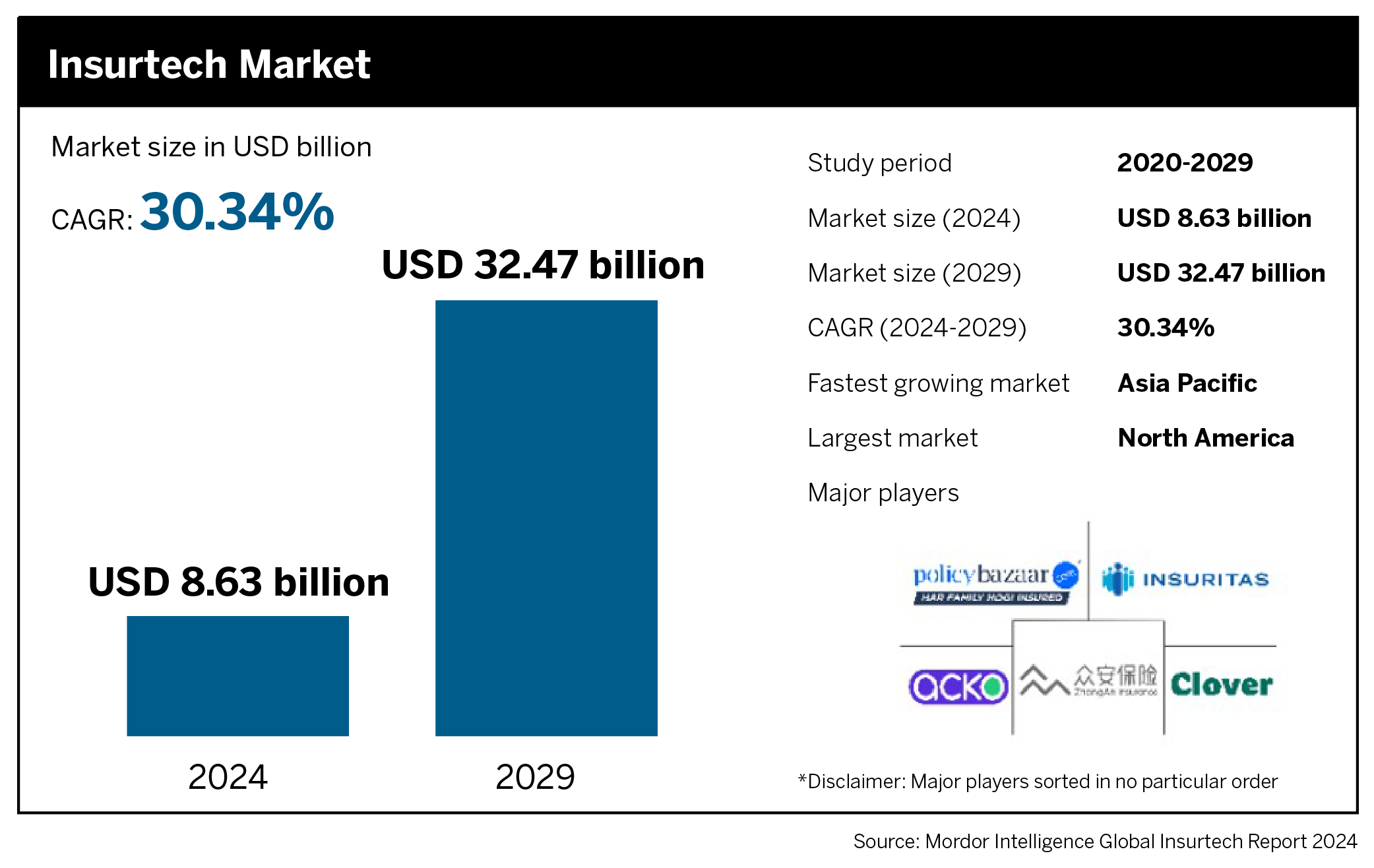

For decades, the German insurance landscape has been defined by a specific kind of cultural reliability: the steady, predictable presence of the legacy provider. In a society that prizes stability and risk aversion, the Privathaftpflicht Versicherung (private liability insurance) has evolved from a recommended safety net into a virtual necessity for millions of households across Germany, Austria, and Switzerland.

However, the arrival of “Insurtech” disruptors—companies like Lemonade that promise a purely digital, AI-driven experience—has forced a reckoning for the industry’s giants. The tension between traditional reliability and digital agility is now the primary battlefield for market share. At the center of this shift is HDI Versicherung and its parent company, Talanx AG, which is currently attempting to prove that a “hybrid” model—combining human expertise with digital efficiency—is the most sustainable path forward.

For the average consumer, this corporate tug-of-war manifests as a choice between the lean, app-based interface of a startup and the comprehensive, advisor-led support of an established firm. While the allure of a five-minute digital signup is strong, the complexities of modern risk—ranging from extreme weather events to cyber liabilities—are renewing the demand for the depth of coverage and financial solvency that only larger players can typically guarantee.

The Cultural Necessity of Liability Coverage

In Germany, private liability insurance is not a legal requirement, yet it remains one of the most widely held insurance products. The reason is simple: the potential for catastrophic financial loss. Under German law, an individual can be held liable for damages caused to others for the rest of their life, regardless of their current income. A single accident—a fire caused by a faulty appliance or a serious injury caused by a pedestrian—can lead to claims in the millions of euros.

HDI Versicherung has positioned its Privathaftpflicht Versicherung as a bulwark against this volatility. By offering high coverage limits and expanding policies to include “accident consequence costs,” the provider targets a demographic that values comprehensive protection over the lowest possible monthly premium. This focus on “all-round” security is a strategic move to differentiate itself from budget-focused digital competitors.

Similarly, household insurance (Hausratversicherung) is seeing a resurgence in relevance. As extreme weather events—such as the devastating floods seen in parts of Western Europe in recent years—become more frequent, the require for robust protection against water and fire damage has shifted from a luxury to a priority. HDI’s strategy involves tailoring these tariffs to specific living situations, whether for a renter in a high-density city like Munich or a homeowner in Zurich, integrating app-based claims reporting to reduce the friction of the traditional bureaucracy.

Stability vs. Disruption: The Insurtech Challenge

The rise of the “digital-first” insurance model promised to democratize the industry by removing the middleman. Companies like Lemonade entered the European market with the goal of using artificial intelligence to automate underwriting and claims processing, theoretically lowering costs for the consumer.

However, the German market has proven resistant to a purely digital approach. While growth was initially rapid, some Insurtechs have struggled with declining premiums and high acquisition costs in the DACH region. The “human element”—the ability to speak with a qualified advisor during a complex claim—remains a high-value commodity for German consumers.

HDI has responded not by ignoring digitalization, but by absorbing it. By maintaining a hybrid strategy, they allow customers to toggle between digital tools for simple tasks and human consultants for complex risk assessments. This approach addresses the needs of “risk-averse” clients who aim for the speed of an app but the security of a corporate balance sheet.

Comparative Market Approaches in the DACH Region

| Feature | Traditional/Hybrid (e.g., HDI) | Pure Insurtech (e.g., Lemonade) |

|---|---|---|

| Customer Interface | App + Human Advisor | App-Only / AI Chatbot |

| Risk Assessment | Comprehensive/Manual Review | Algorithmic/Data-Driven |

| Market Stability | High (Backed by Talanx AG) | Variable (Growth-focused) |

| Claims Process | Hybrid (Digital + Case Manager) | Automated/Instant |

Talanx AG: The Corporate Engine

The stability of HDI is inextricably linked to the strategic direction of Talanx AG (ISIN: DE000TLX1005). As the parent company, Talanx operates as a diversified powerhouse covering property, casualty, life, and reinsurance. Its current strategy is one of “balanced growth,” avoiding the aggressive, high-risk expansion often seen in the tech sector in favor of sustainable efficiency.

Talanx has focused heavily on cost control and operational synergy. For the end-user, this efficiency is intended to translate into stable premiums even in an inflationary environment. The group is investing heavily in AI for claims evaluation, which aims to shorten the time between a loss event and the payout without removing the oversight of human experts.

A critical component of Talanx’s resilience is its adherence to Solvency II regulations. This EU-wide framework ensures that insurance companies hold enough capital to survive significant losses, providing a layer of security that smaller, venture-backed startups may struggle to match during a market downturn.

New Frontiers: Climate, Cyber, and Demographics

The insurance industry is currently facing a triad of systemic shifts that are redefining the nature of risk:

- Climate Risk: The increase in natural disasters is driving up loss ratios. To counter this, HDI is refining its products to include expanded coverage for floods and storms, while utilizing reinsurance to spread the risk.

- Cyber Threats: As private lives become fully digitized, the risk of identity theft and digital fraud has grown. This is opening the door for new products, such as cyber-liability extensions for private individuals.

- Demographic Shifts: An aging population in Germany, Austria, and Switzerland is creating a surge in demand for long-term care and health-related insurance, prompting HDI to expand its portfolio beyond simple liability and property coverage.

These shifts require a level of agility that traditionally slow-moving insurance companies have lacked. The success of the Talanx-HDI ecosystem will depend on whether they can integrate these new risks into their policies without pricing out the middle-class consumer.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Stocks and insurance products are subject to market volatility and individual risk profiles.

Looking ahead, the next major checkpoint for the sector will be the upcoming quarterly earnings reports from Talanx AG, which will reveal how effectively the group’s efficiency measures are offsetting the rising costs of climate-related claims. Any updates to EU insurance directives regarding transparency and digital distribution will likely force a further evolution of the hybrid service model.

We invite you to share your thoughts in the comments: Do you prefer the efficiency of an AI-driven app or the security of a human advisor when it comes to your insurance?