The modern factory floor is no longer just a place of heavy machinery and manual labor; it is becoming a sophisticated network of data-driven ecosystems. As the transition to “Industrie 4.0” accelerates, the ability for machines to self-optimize and predict their own failures is shifting from a futuristic concept to a competitive necessity. For investors in the DACH region—Germany, Austria, and Switzerland—this evolution presents a strategic entry point into the global automation trend.

At the center of this shift is Rockwell Automation, a Milwaukee-based powerhouse listed on the New York Stock Exchange. By providing the software and hardware architecture that allows factories to become “intelligent,” the company has positioned itself as a critical bridge between traditional industrial manufacturing and the digital future. For those seeking stable growth in the tech sector, understanding warum Industrie 4.0 Chancen für dich birgt requires a appear at how automation is solving the most pressing problems of the modern European economy.

The company operates under the ISIN US7739031091, offering investors exposure to the core of industrial digitalization. Whereas the stock is traded in US Dollars, its operational relevance is deeply embedded in the European industrial heartland, where the pressure to increase efficiency amid labor shortages and energy costs has never been higher.

The Architecture of the Smart Factory

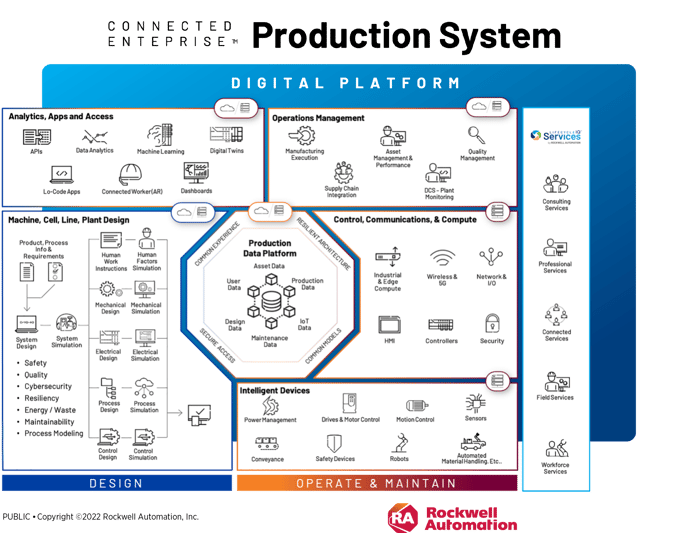

Rockwell Automation does not simply sell equipment; it sells the “brain” of the production line. The company’s business model is built on three primary pillars: Logix controllers, connected enterprise systems, and lifecycle management services. This integrated approach allows a manufacturer to move from a reactive state—fixing a machine after it breaks—to a predictive state, where data analysis warns operators of a failure before it occurs.

A significant strategic pivot in recent years has been the move toward Software-as-a-Service (SaaS) and cloud-based solutions. By shifting from one-time hardware sales to recurring software revenue, Rockwell is insulating itself from the typical volatility of industrial capital expenditure cycles. This scalability is further enhanced by the use of “Digital Twins”—virtual replicas of physical assets that allow engineers to test optimizations in a digital environment before implementing them on the factory floor.

This technological stack is particularly relevant for high-stakes sectors such as automotive, pharmaceuticals, and food and beverage. In these industries, a single hour of unplanned downtime can cost millions of euros, making the demand for Rockwell’s predictive maintenance tools a matter of operational survival.

Official Resource

For the latest corporate filings and technical specifications, visit the official company portal.

Strategic Relevance for the DACH Region

For investors in Germany, Austria, and Switzerland, Rockwell Automation serves as a proxy for the health of the European industrial sector. Germany, as the global hub for mechanical engineering, is currently undergoing a massive digital overhaul. Automation is no longer a “nice-to-have” but a requirement to offset a shrinking skilled workforce and the stringent requirements of the EU Green Deal.

The drive toward sustainability is a primary catalyst. Energy-efficient production systems reduce carbon emissions, directly aligning with European regulatory mandates. By helping companies optimize their energy consumption and reduce waste through precision automation, Rockwell is tapping into a long-term growth driver fueled by ESG (Environmental, Social, and Governance) compliance.

While Rockwell faces stiff competition from European giants like Siemens, it differentiates itself through open platforms that maintain compatibility across diverse systems. This flexibility is highly valued in the Swiss precision industry and the Austrian manufacturing sector, where specialized, high-quality production often requires a mix of different technological providers.

Market Position and Competitive Edge

| Feature | Rockwell Automation | Traditional Hardware Peers |

|---|---|---|

| Core Focus | Integrated Software & Hardware | Heavy Hardware Emphasis |

| Revenue Model | Shift toward Recurring SaaS | Primarily Transactional |

| Key Product | Allen-Bradley / FactoryTalk | Component-based systems |

| Strategy | Lifecycle Automation | Product-specific sales |

Analyzing the Risks and Market Drivers

Despite the strong tailwinds of Industrie 4.0, the investment landscape is not without friction. The most prominent risk is the cyclical nature of the industrial sector. When global GDP slows or recessionary fears peak, companies typically delay large-scale investments in new plant equipment. Monitoring the Purchasing Managers’ Index (PMI) is essential for any investor in this space, as it serves as an early warning system for industrial demand.

Geopolitical tensions also play a role. The trend of “reshoring”—bringing production back to Europe and North America to shorten supply chains—is a net positive for Rockwell. Still, this is balanced against the risk of semiconductor shortages and currency fluctuations, particularly the USD/EUR exchange rate, which can impact the reported earnings for European holders.

From a technical standpoint, the rise of generative AI introduces both an opportunity and a threat. While AI can enhance the predictive capabilities of Rockwell’s software, new software-first entrants could potentially disrupt the traditional hardware-led approach to automation. Rockwell’s strategic partnership with PTC and the integration of tools like ThingWorx are direct attempts to stay ahead of this curve.

Financial analysts generally view the company’s shift toward recurring revenue as a key stabilizer. By locking customers into long-term software contracts, Rockwell creates higher switching costs, making it difficult for clients to migrate to a competitor once their entire lifecycle management is integrated into the Rockwell ecosystem.

Disclaimer: This article is provided for informational purposes only and does not constitute financial advice. Stocks are volatile instruments and carry inherent risks.

As the industry moves forward, the next critical checkpoint for investors will be the upcoming quarterly earnings reports, with a specific focus on software growth margins and the adoption rates of cloud-based industrial services. These figures will reveal whether the transition to a data-driven business model is accelerating as planned.

We would love to hear your perspective: Is your portfolio leaning toward traditional industrial giants or the new wave of automation software? Share your thoughts in the comments below.